Background

The Control of Hazardous Air Pollutants from Mobile Sources (MSAT-II) regulations, published in February 2007, required that refiners and importers produce gasoline with an annual average benzene content of 0.62 percentage by volume (vol%) or less beginning Jan. 1, 2011. In addition, a maximum average standard benzene content for refineries of 1.3 vol% was established with compliance required by July 1, 2012.

This acts as an upper limit on gasoline benzene content when credits are used to meet the 0.62 vol% standard. In response to these regulations, many refiners across the U.S. implemented units to destroy benzene in light reformate streams — typically isomerization units and benzene saturation units. Today, newly commercialized technologies may have additional benefits for refiners in a changing market environment. This may have led refiners to implement a different strategy to reduce benzene content in gasoline streams had the MSAT-II regulations been imposed more recently rather than in 2007.

The U.S. gasoline and benzene market has changed considerably in the past decade. As such, decisions made in 2007 may not be the optimal decision for a refinery that is struggling to meet demand for premium gasoline and experiencing high operating costs today, and new technologies in benzene conversion may contribute to a more cost-effective process. Additionally, refiners may find that a refreshed MSAT-II strategy can be a profitable investment, converting what many considered to be a purely regulatory project in 2007 to a refinery profit improvement project in 2020 and beyond.

Read The White Paper

Background

The Control of Hazardous Air Pollutants from Mobile Sources (MSAT-II) regulations, published in February 2007, required that refiners and importers produce gasoline with an annual average benzene content of 0.62 percentage by volume (vol%) or less beginning Jan. 1, 2011. In addition, a maximum average standard benzene content for refineries of 1.3 vol% was established with compliance required by July 1, 2012.

This acts as an upper limit on gasoline benzene content when credits are used to meet the 0.62 vol% standard. In response to these regulations, many refiners across the U.S. implemented units to destroy benzene in light reformate streams — typically isomerization units and benzene saturation units. Today, newly commercialized technologies may have additional benefits for refiners in a changing market environment. This may have led refiners to implement a different strategy to reduce benzene content in gasoline streams had the MSAT-II regulations been imposed more recently rather than in 2007.

The U.S. gasoline and benzene market has changed considerably in the past decade. As such, decisions made in 2007 may not be the optimal decision for a refinery that is struggling to meet demand for premium gasoline and experiencing high operating costs today, and new technologies in benzene conversion may contribute to a more cost-effective process. Additionally, refiners may find that a refreshed MSAT-II strategy can be a profitable investment, converting what many considered to be a purely regulatory project in 2007 to a refinery profit improvement project in 2020 and beyond.

The Problem With Benzene Destruction via Saturation

After MSAT-II regulations, most refiners chose to install a solution that included two main steps:

- Limiting the amount of benzene produced in the catalytic reformer by removing precursors — such as C6 naphthenes — from the reformer feed.

- Saturating benzene produced in the reformer using a commercially available technology to destroy benzene in the light reformate and light straight-run naphtha.

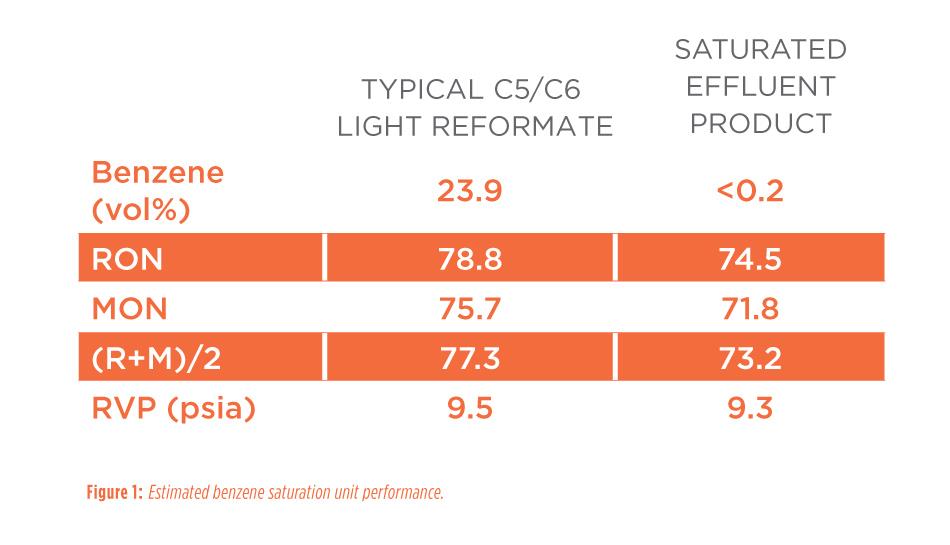

The saturation of benzene is a destruction of octane and a large consumer of hydrogen, which leads to an increase in operating costs and reduction in refinery margin, as shown in Figure 1. Furthermore, if the refinery implements the two steps outlined above and feeds the resultant high-precursor light straight-run naphtha and the low-benzene reformate into an isomerization unit to retrieve lost octane, the resultant feedstock can have a detrimental impact on the overall approach to equilibrium in the isomerization unit due to a high X-factor (defined as feedstock content of C6 naphthenes, benzene and C7+). This further reduces potential octane gain across the downstream unit.

Significant Market Changes Since 2007/2008

Several major changes have occurred to the market since the introduction of the MSAT-II regulations. Changes — such as additional gasoline regulations (Tier III) — have impacted both the benzene supply in the U.S. and octane demand in gasoline pools by affecting the refinery octane balance and creating a shale gas revolution in U.S. petrochemical production. This, in turn, has affected the steam cracker feed slate and the discovery and subsequent processing of shale condensate.

Octane Demand

Octane is in high demand due to three primary contributing factors:

- The Tier III Motor Vehicle Emission and Fuel Standards program, published in April 2014, which set a new gasoline sulfur standard beginning in 2017 for large refiners (>75 mbpd [thousand barrels per day]) and in 2020 for small refiners (<75 mbpd). This regulation reduces the gasoline sulfur average to 10 parts per million (ppm), down from the previous average of 30 ppm.

This reduction in the gasoline sulfur average generally requires post-hydrotreating of the fluid catalytic cracking (FCC) gasoline, whereas some refiners were able to meet previous regulations without post‑treatment. Across these post-hydrotreating units, octane loss due to olefin saturation is experienced depending on the severity of treatment and the olefin content of the gasoline. In refineries with an existing post-treater, the octane loss will generally increase to meet a 10 ppm sulfur average in gasoline pools.

- Increased corporate average fuel efficiency (CAFE) standards may increase the demand for mid-grade and premium-grade gasoline due to increasing engine compression ratios.

- The discovery and processing of shale condensate yields significant volumes of low-octane, straight-run naphtha or natural gasoline. An increase in the availability of low-cost ethane in the U.S. has resulted in a significant feedstock shift away from liquids (naphtha) cracking toward ethane cracking, stranding this low-octane naphtha to be blended into the U.S. gasoline pool once existing octane-boosting units are at capacity limits.

To combat an overall loss in octane, refiners can increase reforming severity. However, this generally will produce more benzene in the light reformate, potentially compounding the existing problems for many refiners.

Benzene Supply

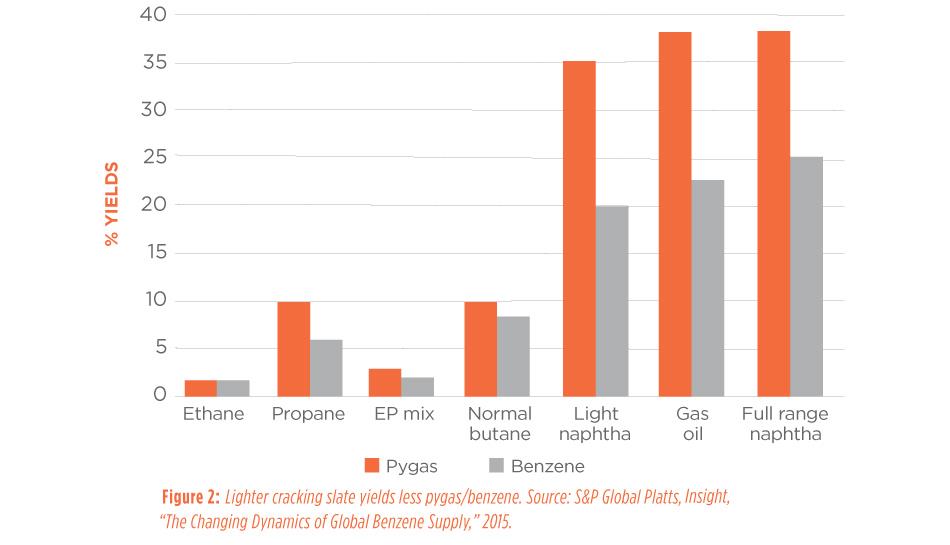

The U.S. steam cracking industry previously processed a mix of natural gas liquids (NGLs), naphthas and gasoils. However, market shift over the last five years, according to S&P Global Platts, has increased the ethane portion of the U.S. cracking slate to more than 90% of the feedstock as the industry moves away from naphtha and gasoil cracking. This shift results in a significant reduction in benzene and pyrolysis gasoline (pygas) yield from steam cracking, evidenced by Figure 2. This shift has affected both the benzene and octane supply markets, as less benzene is being produced from steam cracking, and less pygas — a high-octane gasoline blending component due to the high aromatics content — is available for blending.

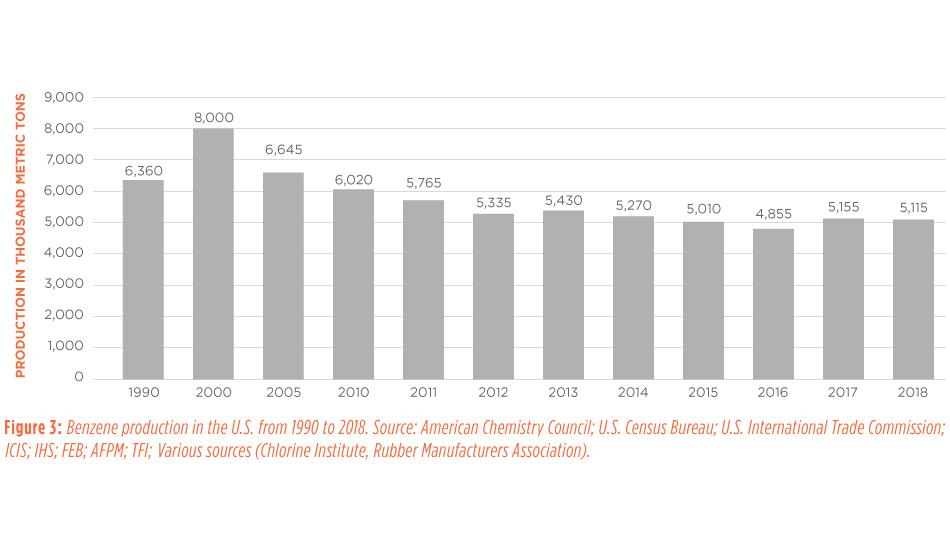

The U.S. is producing only 5.1 million metric tons of benzene per year, as shown in Figure 3. This is down from 8 million metric tons per year in 2000, meaning the U.S. is now importing much of this differential, approximately 1.7 million metric tons per year in 2018.

Competing Technologies for Benzene Removal

During MSAT-II compliance studies, other technologies were likely considered before a saturation option was selected. In today’s market, there are commercially proven technologies that can assist a refiner in meeting MSAT-II requirements.

Benzene Alkylation

Benzene alkylation technology itself is not new; this technology has been utilized for many years to produce cumene. However, this technology has recently been commercialized to process a benzene-rich feedstock such as C5/C6 range light reformate into a stream containing corresponding branched aromatic analogues of benzene by reacting with ethylene or propylene.

In other words, a light reformate stream can be fed to a benzene alkylation unit directly, converting the benzene into other molecules that satisfy the MSAT-II regulation while also increasing the octane and reducing the Reid vapor pressure (RVP) of the resultant stream. As noted, a light-olefin stream is required as a reactant; however, these streams are bountiful and relatively inexpensive in certain parts of the U.S. today, especially the U.S. Gulf Coast.

Another advantage of this process is it may be possible to retrofit an existing benzene saturation unit into a benzene alkylation unit with modifications.

It should be noted that the endpoint of the gasoline component will be much higher than the feedstock due to heavy aromatics production. Refiners must be careful to see that the resultant stream will continue to meet specifications when blended into the larger refinery pool.

Dividing Wall Column

Dividing wall columns (DWC) combine two or more distillation columns within a single shell to enable three or more products to be separated from a feed stream. Applied to a reformate stream, a DWC can produce a benzene-rich stream and an MSAT-II-compliant benzene-lean stream intended for direct gasoline blending. The benzene-rich stream can then be processed separately, reducing overall operating costs. This technology boosts savings in both energy consumption and total distillation column area as compared to separate columns.

There are multiple commercial examples of DWC technology being employed as part of an overall MSAT-II compliance solution.

Benzene Extraction

In the right circumstances, benzene extraction via extractive distillation may be a profitable option for refiners if there is an adequate volume of benzene-rich streams available to justify investment. The U.S. is currently importing significant volumes of benzene, as benzene production from naphtha cracking diminished significantly between 2015 and 2020. Furthermore, refiners may be able to sell a tightly fractionated benzene-rich stream from reformate to petrochemical producers who have spare extraction capacity available today.

Conclusion

In the changing U.S. gasoline and benzene market, decisions made by refiners in 2007 may no longer be optimal in helping a refinery meet today’s demand for premium gasoline and new goals for lower operational costs. Since that time, new technologies in benzene conversion have made it possible to create more cost-effective processes. By refreshing MSAT‑II approaches, refiners can now profit from the investment made in 2007, converting their regulatory projects to an improvement program that will produce profits today and in the future.

.svg)