Global Crude Oil and Petrochemical Growth Today

Gasoline, diesel, jet fuel — these are the primary products that come from crude oil. However, the world market for these products is currently exhibiting flat to slow growth of around 0.7% to 0.9% yearly. This is due in part to the impacts of traditional fuel replacement — including market penetration of methanol, ethanol and liquified natural gas (LNG) — plus slow but steady increasing electrification of the transportation fleet and mandated improvement in global fuel efficiency standards, such as the Corporate Average Fuel Economy (CAFE) Standards implemented in the U.S.

In comparison, the global petrochemical market is growing at nearly 4% per year. But why? There are a multitude of reasons, including worldwide population growth, increasing income and wealth, and aging population in developed areas of the world.

Read The White Paper

Global Crude Oil and Petrochemical Growth Today

Gasoline, diesel, jet fuel — these are the primary products that come from crude oil. However, the world market for these products is currently exhibiting flat to slow growth of around 0.7% to 0.9% yearly. This is due in part to the impacts of traditional fuel replacement — including market penetration of methanol, ethanol and liquified natural gas (LNG) — plus slow but steady increasing electrification of the transportation fleet and mandated improvement in global fuel efficiency standards, such as the Corporate Average Fuel Economy (CAFE) Standards implemented in the U.S.

In comparison, the global petrochemical market is growing at nearly 4% per year. But why? There are a multitude of reasons, including worldwide population growth, increasing income and wealth, and aging population in developed areas of the world.

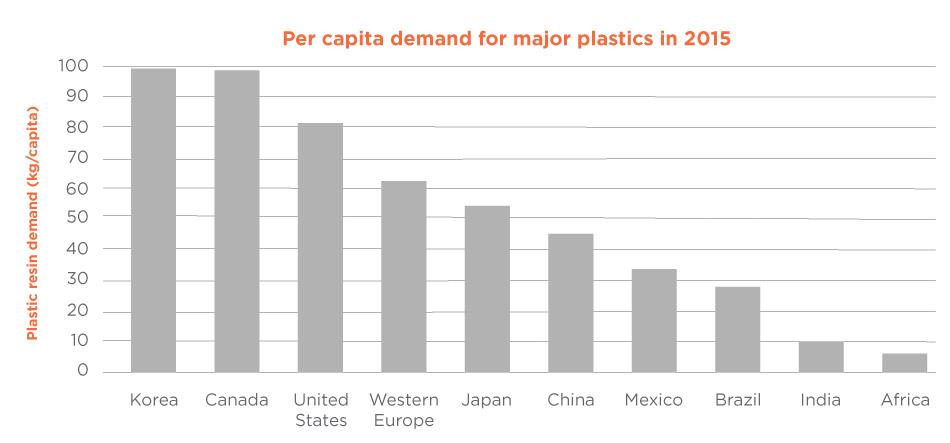

Worldwide Population Growth and Petrochemical Consumption

Many items found in our daily lives — from food packaging to clothes to cars — contain petrochemical products. This consumption is most prevalent in developed areas of the world, including North America and Western Europe, where the consumption of petrochemicals is highest per capita.

As the large population centers of our planet — especially China and India — grow and citizens begin to enter a more middle-class, consumption-based lifestyle via an increase in disposable income, these populations will generally begin to consume more petrochemical-based products. The demand in these areas will increase substantially, dwarfing the consumption currently experienced in North America and Western Europe. Today, demand for petrochemicals in less-industrialized areas of the planet is exploding, doubling every 12 to 15 years.

Meanwhile, demand in parts of the world that are already consuming the most petrochemicals per capita are still strong and growing, albeit for slightly different reasons. For example, in the U.S., the population is beginning to age; the median age in the U.S. has increased from 30 years in 2000 to 38 years in 2018, according to census data. As more of the population enters a retirement lifestyle, their consumption of transportation fuels generally decreases, but their consumption of petrochemicals generally increases. This is due to an accumulation of wealth throughout their working lives, resulting in a highly consumer-driven retirement.

Figure 1: As consumption in China, India, Latin America and Africa approach that of North America and Western Europe, the larger population centers of the world will become the largest consumers of petrochemicals on the planet, thus driving significant demand growth. Source: IEA 2015.

Where Will the Production Come From?

Generally, petrochemicals are produced from natural gas liquids (NGLs), like ethane, propane and butane, and naphtha via various processes to produce both olefins and aromatics — the basic building blocks from which further chemicals are derived. A global abundance of NGLs from shale gas deposits has resulted in a petrochemical boom in various parts of the world, especially the U.S. Gulf Coast. However, steam cracking and dehydrogenation of NGLs is an incomplete chemistry, as it produces only ethylene, propylene and butylene but does not produce adequate quantities of heavier petrochemical products, such as butadiene, benzene and paraxylene. Thus, demand for naphtha to be used as petrochemical feedstock still exists for steam cracking to produce butadiene and benzene or reforming to produce paraxylene.

Oil-to-chemicals complexes can achieve production of many primary petrochemical products as described above. The molecular optimization inside a state-of-the-art oil-to-chemicals complex will allow maximum production of light olefins, as well as heavier petrochemical products resulting in full market coverage, product and revenue diversification, and inherent minimization of market risk.

The Impact of Shale Gas in the U.S. Gulf Coast

From a U.S. perspective, the impact of shale gas on ethylene production is important to note. The U.S. Gulf Coast has added — and is currently adding — significant ethylene capacity due to low-cost feedstock abundance. Most of the new petrochemical capacity produced on the U.S. Gulf Coast will be exported to demand centers in Asia, especially primary ethylene-based commodity chemicals.

U.S. petrochemical producers have a significant feedstock and production cost advantage when it comes to ethylene. However, new oil-to-chemicals complexes will generally also produce significant amounts of ethylene, increasing risk for overbuilding of ethylene production.

What Does an Oil-to-Chemicals Complex Look Like?

The oil and gas market continues to be incredibly competitive. This is because almost all finished products are fungible, and there is very little difference in end product or quality. These products are easily transportable across the globe. This means that organizations that exhibit competitive advantages in certain geographical sectors can take advantage of growth in other geographies. For these reasons, organizations must continue to consider new production or complexes, and to approach them from a financially focused standpoint.

It is expected that most of the new grassroots oil-to-chemicals complexes will be built in parts of the world where crude oil is bountiful and close to the regions experiencing the highest demand growth. This includes the Middle East and Asia, including Southeast Asia. Generally, these complexes are built to leverage economies of scale while pushing the bounds of proven train capacity for both refining and petrochemical units.

There are many ways to build and focus new oil-to-chemicals complexes — there are literally hundreds of different configurations. If a producer started out with a blank sheet of paper, there would be no way to know what the right configuration would be for the business plan or market. Organizations must go through a configuration development process to maximize the value of each stream. This will present the configuration that suits the organization’s needs.

An oil-to-chemicals complex requires a series of traditional refining steps to prepare the oil fractions for conversion to petrochemicals. Generally, this results in a highly complex refinery configuration with significant levels of conversion. Many processes exist to convert oil fractions directly to some petrochemical products — and these processes will be heavily favored during the configuration of an oil-to-chemicals complex as they reduce the steps from oil to petrochemicals, saving capital and operational expenditure. One such example is a high-olefin FCC process, which can produce significant quantities of propylene and butylene.

There are steps a development partner can perform to maximize the internal rate of return (IRR) of the organization’s investment on a new facility. Net present value can be somewhat misleading when options of varying capital spend are compared. Thus, IRR or profitability index (profitability relative to capital spend via net present value) are used to measure or rank different configurations.

Depending on the price set and market demand, as the conversion from fuels to petrochemical products increases, IRR will generally increase. However, at some point, the maximum value of all streams in the plant are achieved, striking a balance between transportation fuels and petrochemical production. In this scenario, further increase of petrochemical production will begin to erode the complex’s value. Methodologies can be applied to determine this maximum point to find the most productive configuration.

Measuring the Economics

There are two ways to measure the economics of new complexes. The first is to measure straight project IRR, looking at a profitability index. It has been seen that oil-to-chemicals complexes have a positive IRR above those expected for a new export refinery investment.

There are economies of scale in building both a refinery and petrochemical plant together. And by “optimizing molecules” in the production process, there are ways to boost the IRR of the project or conversion.

The second way to measure the economics is to measure the complex’s or production’s competitiveness as compared to other routes to the same petrochemical products, such as traditional routes versus an oil-to-chemicals route. Typically, if an organization can figure cost of production then it can optimize the process or project to get the highest return.

Conclusion

The petrochemical market is set to grow quickly while the crude oil market exhibits stagnant to slow growth. Some organizations must become vertically integrated to take production from crude oil to chemicals to maintain a competitive edge and find a disposition for their crude oil production.

New complexes are still being built and this will continue to impact the global market. Today, there are a surprising number of publicly announced complexes. These projects are continuing to take place, and they are happening all over the world. Despite the initial cost of a new complex, organizations are still building them to take advantage of the changing global market.

There are ways to make the most of an organization’s investment — it just takes a full understanding of the market conditions specific to the project and the overall market around the world.

Organizations need to meet local or export demand requirements for fuel and petrochemical products. This means optimizing the balance between product production and properly configuring the process. Partnering with a team that utilizes market knowledge and an understanding of market drivers can help take advantage of opportunities and gain a competitive advantage.

.svg)